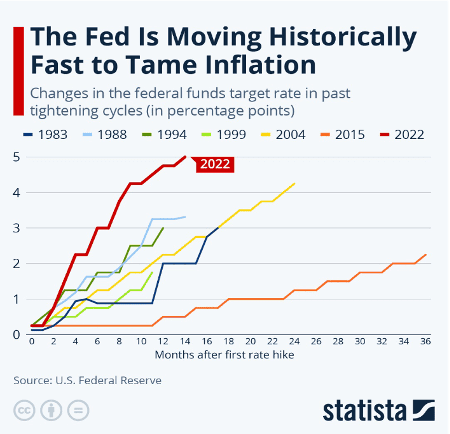

Over the last 18 months, the Federal Reserve raised rates to fight inflation, resulting in a 500+ basis point increase. This represents the most significant rate hike in 35 years.1 This surge raised capital costs substantially, eroding profits and jeopardizing livelihoods. During this time, K1 pursued hedging strategies to help founders and investors mitigate this risk.

Our approach allowed us to hedge approximately 80% of our debt across the portfolio at an average base rate of 4.25%2 compared to the current SOFR3 rate of 5.413%. These strategies have saved our portfolio companies approximately $27 million in annual interest expense4, freeing up resources to invest in people, products, and growth.

In this article, we’ll share the tactics we employed to help founders, executives, and investors mitigate the negative effects of rising interest rates on their companies.

Feeling Squeezed? You’re In Good Company

If you are squeezed in the current environment, you’re not alone. Rate hikes affect many players in our economy—from consumers to banks to business owners.

For example:

- The sudden rise in interest rates have been a significant factor in the challenges faced by banks, including Silicon Valley Bank, Signature Bank, and First Republic Bank.5

- KBRA estimates nearly 15% of mid-market companies cannot meet their interest rate payments.

- Through April of this year, there were over 250 corporate bankruptcies and defaults—a level not seen since 2010.6

The good news is that while rates remain high, there are methods you can employ to combat them. Enter swaps and caps.

Understanding Swaps and Caps

Swaps and caps are valuable tools that can allow you to mitigate risk in—and sometimes even profit from—a rising interest environment.

Understanding Caps

A cap is essentially an insurance product that limits the interest rate you’ll pay on your variable-rate credit. You pay a premium for the product now, and in exchange, you’ve set a limit (or a “cap”) on your interest rate.

You would purchase a cap when you predict that interest rates will increase above a threshold you are comfortable paying, and you have the excess cash now to purchase the “insurance policy”.

Another reason to buy a cap is that you are still paying the floating rate. Meaning, if rates go down, you benefit from paying the lower rate while still having the insurance policy in place. If rates exceed your cap, you only pay the capped rate. See two example scenarios below:

| Scenario 1 – Rates Increase (Cap is met) | Scenario 2 – Rates Decrease (Cap is not met) | |

| SOFR | 5.5% | 3.5% |

| SOFR Cap | 5.0% | 5.0% |

| Loan | $100 | $100 |

| Your Interest Expense | $5.0 | $3.5 |

Understanding Swaps

A swap is a derivatives product where you can exchange a floating for a fixed interest rate. When facing volatility like we have the past 24 months, this can provide significant savings.

Revisiting our scenario from above, regardless of whether the Fed raises or lowers rates, you still pay 4%:

| Scenario 1 – Rates Increase | Scenario 2 – Rates Decrease | |

| SOFR | 5.5% | 3.5% |

| Interest Rate Swap | 4.0% | 4.0% |

| Loan | $100 | $100 |

| Your Interest Expense | $4.0 | $4.0 |

How We Use Swaps

Our Debt Capital Markets (DCM) team helps secure swaps for portfolio companies when we see opportunities to reduce uncertainty and volatility. Swaps are the primary instrument we have used in 2023.

In early 2023, the forward yield curve implied interest rate declines in the second half of 2023, despite the Fed’s stated intent to continue raising and maintaining high rates.

Because of this inverted yield curve, we had the opportunity to both fix our interest rates at a set level, and to reduce the rate we were paying. And on the downside, if rates did indeed fall precipitously – lower rates would imply higher software valuation multiples, offsetting the potential downside to fixing our rates. Through a series of swaps, we were able to hedge our portfolio companies’ base rate on their debt at ~4.25% vs. a SOFR rate of 5.41%, saving approximately $27M annually.7

Mike Cagle, CFO at Smarsh, reflected: “Swaps are easy to overlook, and something most of us don’t consider as operators. K1’s hedging strategy and guidance from the DCM team saved us millions over the last 6 months.”

“Swaps are easy to overlook, and something most of us don’t consider as operators. K1’s hedging strategy and guidance from the DCM team saved us millions over the last 6 months.”

Mike Cagle, CFO, Smarsh

Why We Invest in an In-House DCM Team

The answer to this question is straightforward: We want to find opportunities to generate above-market returns for our companies and investors, viewing a dedicated DCM team as a competitive edge in achieving this objective.

| The Benefit of In-House DCM Bringing DCM in-house allows us to monitor markets in real-time. Our portfolio companies act faster to capitalize on changes in the debt market. |

Many PE firms are simply too small to absorb the cost of this kind of team. As a 135+ person firm with a focused investment thesis in B2B software, we are uniquely positioned to make this investment, and it ultimately provides us all better returns.

Jason Pletcher, COO of GoCanvas, highlights the value: “Putting the swap in place has been hugely valuable in terms of our ability to effectively manage cash in this rising-rate environment. It would have taken us much longer to execute on our own if we did not have the expertise and connections of K1’s DCM team on our side.”

Summing It Up

Swaps and caps are easy to overlook – especially when interest rates are low. However, these hedging strategies are a great tool to put some control back in a company’s hands, which is not easy to come by in today’s environment.

If you are part of a management team dealing with potential/ongoing debt financing, we strongly recommend considering the strategies outlined above. If you’re in the software space and interested in learning about K1 and our resources, don’t hesitate to reach out. We’re happy to brainstorm and share our experiences.